Managing money doesn’t have to feel like solving a complicated math problem while your coffee gets cold.

The truth is, budgeting is simply telling your money where to go instead of wondering where it went. Whether you’re saving for a vacation, paying off debt, building an emergency fund, or just trying to stop your paycheck from disappearing a few days after payday, a good budget can make life a whole lot less stressful.

The best part? You don’t have to give up every little joy or survive on instant noodles to make a budget work. A realistic budget should fit your lifestyle, not make you dread checking your bank account.

In this guide, you’ll discover practical budgeting tips that are easy to follow, flexible enough for real life, and effective for reaching your financial goals.

Why Budgeting Matters

A budget is simply a plan for your income and expenses over a specific period, usually a month. It helps you:

- Understand where your money goes.

- Reduce unnecessary spending.

- Save consistently.

- Prepare for unexpected expenses.

- Reach financial goals faster.

- Reduce financial stress.

Many people avoid budgeting because they think it means saying “no” all the time. In reality, a budget lets you spend on what matters most while cutting back on things that don’t bring much value.

Start by Knowing Your Income

Before creating a budget, know exactly how much money comes in each month.

Include all reliable income sources, such as:

- Salary or wages

- Freelance income

- Side business earnings

- Rental income

- Government benefits, if applicable

If your income varies monthly, calculate your average monthly income using several recent months. It’s usually safer to budget with your lower average income rather than your highest-earning month.

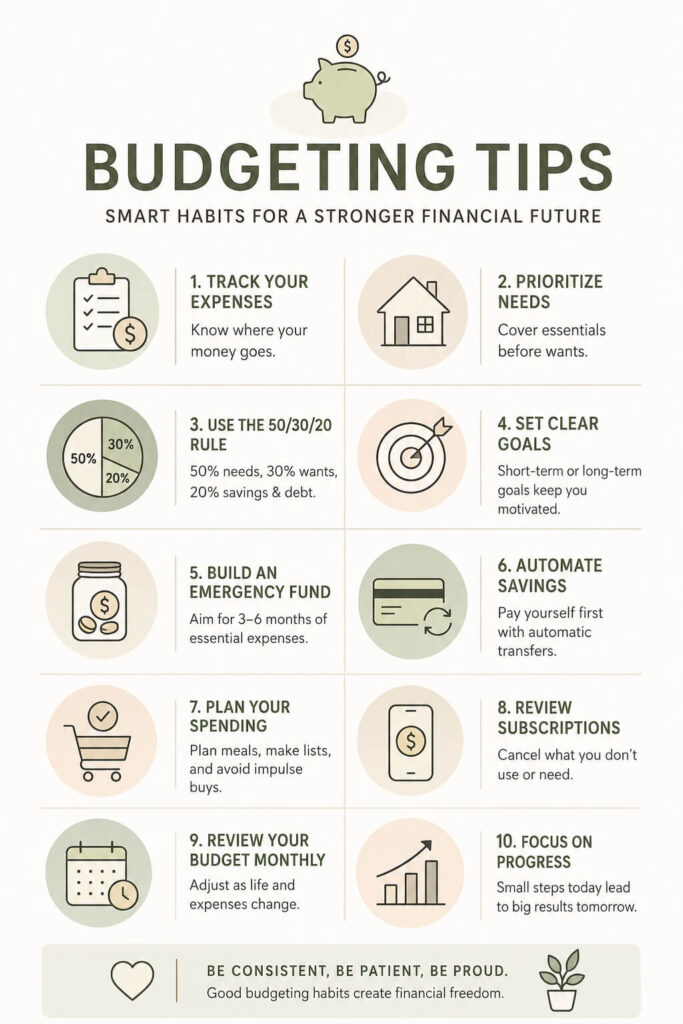

Track Every Expense

One of the most valuable budgeting tips is to track your spending before trying to change it.

For at least one month, write down every expense.

This includes:

- Rent or mortgage

- Utilities

- Groceries

- Transportation

- Insurance

- Dining out

- Coffee runs

- Online subscriptions

- Entertainment

- Shopping

Yes, even that late-night online purchase that somehow seemed completely necessary at 1 a.m.

Tracking expenses helps you identify spending habits and areas where you can save without feeling deprived.

Separate Needs From Wants

A helpful budgeting exercise is dividing expenses into two categories.

Needs

These are essential expenses that keep daily life running.

Examples include:

- Housing

- Utilities

- Groceries

- Transportation

- Insurance

- Basic healthcare

Wants

These improve your lifestyle but aren’t necessary for survival.

Examples include:

- Streaming subscriptions

- Restaurant meals

- Premium coffee

- New clothes beyond essentials

- Hobbies

- Entertainment

This doesn’t mean eliminating every want. Instead, it helps you make intentional spending decisions.

Try the 50/30/20 Budget Rule

One of the most popular budgeting methods is the 50/30/20 rule.

Here’s how it works:

- 50% of income goes toward needs.

- 30% goes toward wants.

- 20% goes toward savings and debt repayment.

This framework works well for many households, although your percentages may differ depending on your financial situation or local cost of living.

The important part is giving every dollar a purpose.

Set Clear Financial Goals

Budgeting becomes much easier when you know what you’re working toward.

Examples include:

Short-term goals

- Build a $1,000 emergency fund

- Save for holiday gifts

- Pay off a credit card

- Take a weekend trip

Long-term goals

- Buy a home

- Save for retirement

- Start a business

- Pay for higher education

- Reach financial independence

Specific goals provide motivation when it’s tempting to spend impulsively.

Build an Emergency Fund

Unexpected expenses happen.

Cars need repairs. Appliances stop working. Medical bills appear at the worst possible time.

An emergency fund helps prevent these surprises from becoming financial disasters.

Many financial experts recommend saving three to six months of essential living expenses. If that feels overwhelming, start with a smaller goal, such as saving your first $500 or $1,000.

Small wins build momentum.

Automate Your Savings

One of the easiest budgeting tips is making saving automatic.

Set up automatic transfers from your checking account to your savings account shortly after payday.

When the money moves automatically, you’re less likely to spend it first.

Think of it as paying your future self before anyone else gets the chance.

Use Budgeting Apps or Simple Spreadsheets

Choose a budgeting method you’ll actually use.

Popular options include:

- Budgeting apps

- Spreadsheet templates

- Printable budget planners

- Notebook tracking

- Digital note-taking apps

The best budgeting system isn’t necessarily the fanciest one. It’s the one you consistently stick with.

Plan Meals Before Grocery Shopping

Food spending often takes a surprisingly large bite out of the budget.

Meal planning can help reduce waste and unnecessary grocery trips.

Try these ideas:

- Plan meals for the week.

- Make a shopping list.

- Avoid shopping while hungry.

- Buy pantry staples in appropriate quantities.

- Use leftovers creatively.

You’ll often spend less and waste less food.

Related Read: Money-Saving Techniques: How to Slash Monthly Bills Without Giving Up Comfort

Review Subscriptions Regularly

Subscription services are sneaky.

A few dollars here and there can quietly add up to a significant monthly expense.

Review every recurring payment.

Ask yourself:

- Do I still use this?

- Is there a cheaper option?

- Can I pause it for a while?

Canceling unused subscriptions can free up money with almost no impact on your lifestyle.

Give Yourself Fun Money

A budget that’s too strict rarely lasts.

Set aside a reasonable amount each month for guilt-free spending.

This can cover:

- Coffee

- Books

- Movies

- Hobbies

- Dining out

- Small treats

Enjoying your money is part of healthy budgeting.

Avoid Impulse Purchases

Impulse buying can quickly derail a budget.

Before making non-essential purchases, try waiting at least 24 hours.

For larger purchases, wait several days.

Often, the excitement fades, and you’ll realize you didn’t really need the item after all.

Your shopping cart doesn’t have feelings. It won’t be offended if you leave.

Pay Bills on Time

Late payments can result in:

- Late fees

- Higher interest charges

- Damage to your credit history

Set calendar reminders or automate payments whenever possible.

Staying organized saves money.

Use Cash for Problem Spending Categories

If you tend to overspend in certain areas, consider using cash.

Common categories include:

- Dining out

- Entertainment

- Shopping

- Personal spending

Once the cash is gone, you’ve reached your spending limit for that category.

This simple method makes overspending much harder.

Budget for Irregular Expenses

Not every expense happens monthly.

Don’t forget to plan for:

- Annual insurance premiums

- Holiday gifts

- Vehicle maintenance

- School expenses

- Birthdays

- Home repairs

- Travel

Setting aside a little each month prevents these predictable expenses from becoming financial surprises.

Check Your Budget Every Month

Life changes.

Income changes.

Expenses change.

Your budget should change too.

Review your budget monthly and adjust it based on:

- New bills

- Salary increases

- Financial goals

- Seasonal expenses

- Lifestyle changes

Budgeting isn’t something you create once and forget.

Focus on Progress, Not Perfection

Nobody sticks to a budget perfectly every month.

Unexpected expenses happen.

Sometimes you’ll overspend.

Sometimes you’ll save more than expected.

The goal isn’t perfection. The goal is to make better financial decisions more consistently over time.

Small improvements can add up to meaningful financial progress.

Common Budgeting Mistakes to Avoid

Even well-intentioned budgets can fail if you make these common mistakes.

Making Your Budget Too Restrictive

If your budget leaves no room for enjoyment, you’re less likely to stick with it.

Allow yourself reasonable flexibility.

Forgetting Small Purchases

Daily spending can add up quickly.

Small purchases matter more than many people realize.

Ignoring Irregular Expenses

Planning only for monthly bills creates unnecessary financial pressure later.

Not Reviewing Your Budget

Budgets should evolve with your life.

A yearly review isn’t enough for most people.

Giving Up After One Bad Month

One overspending month doesn’t mean you’ve failed.

Adjust, learn from it, and keep going.

Frequently Asked Questions About Budgeting Tips

What is the easiest way to start budgeting?

Start by tracking your income and expenses for one month. Once you know where your money is going, create spending categories and set realistic limits.

How much should I save every month?

The amount depends on your income and financial goals. Even saving a small percentage consistently can make a difference over time. If possible, increase your savings as your income grows.

Should I budget if my income changes every month?

Yes. Use your average monthly income or budget based on your lowest expected monthly income. Adjust your spending as needed when your earnings vary.

Is budgeting only for people with debt?

No. Budgeting helps everyone, regardless of income or debt level. It’s useful for saving, investing, planning major purchases, and reducing financial stress.

How often should I update my budget?

Review your budget at least once a month. Update it whenever your income, expenses, or financial goals change.

Final Thoughts

Learning good budgeting habits doesn’t happen overnight, but every small improvement can strengthen your financial future.

The best budgeting tips aren’t about making life less enjoyable. They’re about making your money work harder for the things that matter most to you.

Start with one or two changes instead of trying to overhaul your entire financial life in a single weekend. Track your spending, set realistic goals, save consistently, and review your progress each month.

Over time, those simple habits can lead to greater financial confidence, more savings, and fewer money-related surprises. That’s a budget worth sticking to.

Follow me on:

Leave a Reply